Nowhere to hide?

Are there any safe havens for investors? Further thoughts on "Risk Off".

Latin America’s advantages as risk perceptions shift.

Not just a potential global energy crisis, but possible food shortages too.

Peace in Iran seems unlikely, for now at least.

Stock markets are complacent about the risks.

No safe haven so far, but some things are still better than others.

Reminding myself of a painful mistake that I made during the Global Financial Crisis.

A growing risk that is being mostly ignored.

The war in the Middle East has the potential to turn the world’s economies on their heads. The implications for financial markets are huge.

Actually, it’s really two wars. There’s the Iran war spreading around the Persian Gulf. And then there’s the war being waged by Israel in southern Lebanon, against the Iran-supported Hezbollah group. But the reality is that only the first conflict has global implications.

For my comments about the risks from earlier in the week, see “Risk Off” time. Today I’ll expand on those thoughts.

Latin America’s advantages

Before I get into the big stuff, a note on what’s happening here in Argentina, where I live. It puts the risks in the world into perspective. At the most macro level, perceptions of relative risk are shifting, along with actual risk levels.

Everyone “knows” that Argentina is a perennial economic and financial basket case, and has been for decades. Except that this is changing fast, under the leadership of President Javier Milei. Big government is out, more freedom is in, and there’s big investment ongoing into commodity production (drilling, mining).

In a world where global supplies of oil, natural gas, fertiliser, and thus food are all under threat of prolonged shortages, Argentina suddenly looks like a relative safe haven (along with some other countries in resource-rich Latin America).

Argentina’s oil & gas production has boomed in recent times, now putting the country in the position of being a net energy exporter, and with production still growing quickly. It’s also said that the country exports enough food to feed around 240 million people (some say 400 million), on top of domestic demand. Which is to say around five times its own population. (Although, in reality, a lot of the crop exports are used as feed for livestock, so the link is indirect.)

That said, according to a report I found, Argentina imports around 60% of its fertiliser needs. And fertiliser shortages would mean lower crop yields. Most of those Argentine imports come from Morocco, China, the USA and Peru. If there are global fertiliser shortages, even Argentina could face shortfalls.

Something that’s surprised me recently - and an example of markets being turned on their head - is the strength of the Argentine peso. It’s actually up nearly 6% against the US dollar year-to-date. This is practically unprecedented in a time of great market uncertainty.

Usually, as financial crises gather steam, I’d expect the peso to collapse as speculators dump all global assets that are seen as “risky”, including things such as Argentine stocks and bonds. You’d expect that to put pressure on the peso.

This time, so far at least, it’s been different. Most likely due to the aforementioned reasons being set to result in larger export income (dollar inflows) as energy and food commodity prices rise, and possibly with some Argentine central bank intervention thrown in.

The Argentina of the past had a habit of starting crises. This time it looks set to benefit. Much of the rest of Latin America would benefit too, given its geographical location and rich resources. Although it’s only one factor for investors to consider. Politics in individual countries being the other main one, most of the time.

Are we on the cusp of twin global energy and food crises?

Since the war erupted in Iran and the Persian Gulf, most of the focus has been on potential shortages of oil and natural gas, given the large share of global supplies that pass through the Strait of Hormuz.

But nitrogen fertilisers, such as urea, are a specific issue that more and more people are noticing. They’re made using ammonia that’s derived from natural gas. They’re important inputs into the production of wheat, maize (corn), and barley.

Thus, shortages of nitrogen fertilisers could have a big impact on global farming.

Crop shortages would mean higher prices, and potentially even hunger. Especially in the many densely-populated poorer countries that are heavily reliant on fertiliser and/or food imports.

Within the countries around the Persian Gulf itself, food shortages are also a potentially big problem. Arid deserts are not renowned for being fertile. Hence these countries have to import vast amounts of food. How does it all get there if the Strait of Hormuz remains closed?

An energy crisis is one thing, with major implications for economies and financial markets. But a food crisis could spell a humanitarian catastrophe, and provoke major political instability if people start going hungry. There’s no way of guessing the potential consequences around the world.

The regions most exposed to energy and food shortages are Europe, Asia and Africa. Basically, places that need to import a lot of oil, gas, fertiliser, and food.

Iran latest

My last article (”Risk Off” time) began thus: “The world could be on the cusp of the biggest economic and financial meltdown since the Global Financial Crisis (GFC).”

Nothing that’s happened since has changed my mind.

Admittedly, as soon as it was published the US President said he would pause strikes on Iran for five days, and issued a 15-point list of demands to Iran. Markets calmed down, albeit briefly.

In turn, Iran issued its own 5-point list. There is little common ground between the two sides. The US claims it is negotiating with Iran, using intermediaries in Pakistan. Iran said that the US is “negotiating with itself”. Markets got worried again.

The pause on striking Iran was meant to expire on Saturday. Now it’s been extended for another ten days by President Trump, and there may be some talks between the two sides. But markets don’t seem to have bought the promises this time, and the sell-off in stocks and bonds has resumed.

Meanwhile, there are reports of a US troop build-up in the region, which doesn’t bode well for imminent peace.

There’s no certainty here, and we can only guess at outcomes. The war could get worse and last for many months more, or even drag into years (remember Afghanistan). Or there could be a sudden reaching of terms, and rapid de-escalation.

Given that Iran is run by religious fanatics, it doesn’t seem wise to assume that they will be motivated mainly by economic matters. If they see the threat as existential, they could dig in for years.

It’s worth also noting the potential risk to the el-Mandab Strait. That’s the southern transit point into and out of the Red Sea, with the Suez Canal running through Egypt into the Mediterranean Sea to the north. This is another crucial trade route, and Saudi Arabia has already switched a lot of outbound oil exports to this side of the country, given the closure of the Strait of Hormuz to the east.

Iran supports the Houthi rebels in Yemen, which sits alongside El Mandab. Shipping disruption there could prevent larger tanker ships - Ultra-Large Crude Carriers (ULCCs) and Very Large Crude Carriers (VLCCs) - from shipping Saudi oil to Asia and elsewhere. That’s because they don’t fit through the Suez Canal to the north.

What’s more, shipments of manufactured goods on their way to Europe from Asia could be disrupted. The alternative route is to go all the way around Africa.

On balance, my own base case assumption is that nothing will be resolved in the immediate future. Meaning that’s what I believe has the highest probability based on the public information currently available, gleaned from a wide range of sources.

But that’s only a best guess, and could change suddenly.

Market risks remain high, and investors should act accordingly. But everyone should be ready to jump back into stocks if the war ends suddenly and oil & gas prices drop in response.

And if you own oil & gas stocks, you might need to get out of them again tout de suite (i.e. right away). Although I suspect that post-war prices will be higher than pre-war, not least due to the degradation of infrastructure around the Persian Gulf.

I already have my priority stock buy list drawn up and ready. Most of it consists of stocks where I took profits or cut risk in recent days and weeks. In other words, things that I want to own for the long run, but that I’ve tactically retreated from in the short run.

A look at markets

To be clear, I think that the reaction in stock markets has been extremely muted so far. That’s given the potential for major carnage in the global economy that would be caused by prolonged shortages of oil and gas, let alone food shortages.

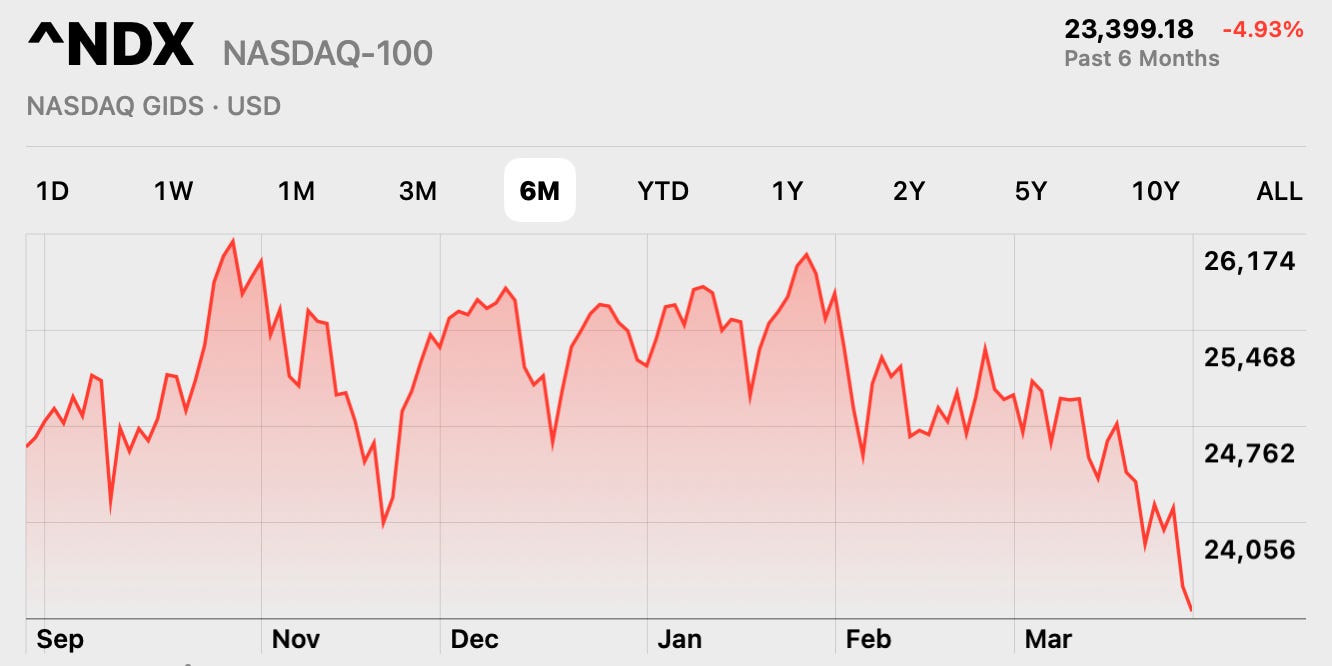

For example, let’s look at the NASDAQ 100 index over the past six months.

Source: Stocks (an app)

It’s down 10.4% since the October peak, which really isn’t much in the grand scheme of things. But the sell-off does appear to be accelerating in recent days.

As mentioned many times on these pages, the US stock market is extremely expensive by any measure, set against both its own history and against other major stock markets.

A lot of the largest companies make big chunks of their profits outside the US, including the “Mag 7” stocks. This means that even if the US economy is relatively insulated from global problems (e.g. due to large domestic food and energy production), US multinational profits are still exposed to recessions elsewhere, and weakening of currencies relative to the US dollar.

Then there are the growing fears that too much capital expenditure is being thrown at AI projects, including vast data centres, with little sign that future revenues will justify the spend.

Throw in the prospect of higher electricity prices in what is an energy-hungry activity. And fears that, even if the suppliers of AI won’t make much money any time soon, many other existing businesses could be upended by AI adoption (e.g. software). And growing concerns about bad debts in the approximately $1.8 trillion private credit lending business, that could have knock-on effects for investors such as the life insurance companies and pension funds that have invested in private credit funds.

Put it together, and the incipient energy crisis could be the final straw for overpriced US stocks. Every bubble bursts eventually. It just needs a pin.

Other stock markets are at risk too, but have also shown a strangely muted response to the obvious risks. It feels like market complacency reigns supreme for now. Many people are concerned, but not as much as they probably should be. But that could change suddenly, potentially morphing into a panic.

Meanwhile, government bond yields are rising, which is to say that bond prices are falling. Developed government finances are already overstretched, and potential recessions (lower tax revenues) or splashing out on populist energy subsidies could make them even worse.

(Incidentally, if you own stocks of power utilities then caution is warranted. Governments can and will impose electricity price caps if things get bad enough. Because of their nature, utility stocks - and for that matter infrastructure funds that invest in this sector - come with a meaningful dose of political risk.)

The situation is also causing gyrations in currency markets. Which means that temporarily parking capital in cash deposits or near-cash investments (treasury bills or very short-dated bonds) isn’t risk free. Especially if we see another spate of money printing to prop up government bond markets (i.e. central banks creating new money to buy government bills or bonds, via the process known as quantitative easing, or “QE”.)

At the same time, the gold price has fallen in recent weeks. Although that was after a huge run in the past couple of years. To keep things in perspective, at $4,523 per troy ounce at the time of writing, the gold price is down about 17% from its intraday January peak, but still at the same level as 9 January, and up 47% over the past year.

That said, gold is up 3% today as I write (Friday). Is it about to stabilise, and even start to rise again? That’s something to watch.

As for crypto, Bitcoin rose initially once the conflict started, but is now falling hard. Many people think Bitcoin is a haven, but I doubt it if there’s a generalised “risk off” market panic. It’s more likely to move in a similar direction to tech stocks, as it has in the past.

If the latter dumps, then I’d expect Bitcoin to as well. Especially if leveraged investors have to sell anything to meet their margin calls (i.e. brokers calling in the debts as the prices of asset collateral fall).

Nowhere to hide?

Stocks down.

Bonds down.

Gold down.

Bitcoin down.

Non-dollar currencies down.

Even the Swiss franc, which is usually a haven of tranquillity, is down 3% against the US dollar since the war started a month ago.

Is there nowhere to hide for investors?

I have some further thoughts about that, at least partly informed by a painful experience during the Global Financial Crisis.