Why oil prices could leap higher

Why oil prices could leap higher

Ignored conflict risks could create a bottleneck for this crucial energy source

The world is full of surprises. Sometimes good, sometimes bad.

The developing situation in Israel and the Gaza strip is clearly horrendous. Unarmed civilians, even children and babies, have been slaughtered by armed groups.

Apparently, the esteemed (?) BBC has refused to call Hamas a "terrorist" organisation. Well, I'll go further. I'll call them war criminals. In my book, murdering undefended children and their parents can be described in no other way.

I don't want to get into the ins and outs of the history of Israel and who is in the right or in the wrong over territorial claims. After all, I have a "minimum politics pledge" to readers, and I'm also no expert on the political and cultural Rubik's Cube of the Middle East.

But that doesn't mean that those faraway events can't have major impacts on the rest of the world. After all, this is the Middle East that we're talking about, which is the world's largest oil bunker.

Israel has no choice but to react the attacks, by moving into the Gaza strip to go after Hamas. But other terror groups may be inspired, including Hezbollah in Lebanon, which is to Israel's north. What's more, I just read that Israel has bombed airports in Syria, apparently to strike at Iranian arms shipments. Syria also borders Israel's north-west. And the US is sending in at least two aircraft carrier groups to the Mediterranean Sea.

That already sounds like a highly unstable cocktail of actors that could easily erupt into a largescale regional conflict. But, in terms of global consequences, we need to remember that Iran is the benefactor behind Hamas.

Iran is hundreds of miles away from Israel. But it has a long sea border along the Persian Gulf. (After all, what more or less constitutes modern Iran used to be known as "Persia".)

Most specifically, Iran controls one side of the Strait of Hormuz, which links the Persian Gulf to the Gulf of Oman. This is a narrow sea lane through which a very substantial amount of the world's oil must pass, on its way from Saudi Arabia and other producers such as Kuwait and Iraq.

The clear risk is that Iran takes steps to try to stop or disrupt oil exports from the Persian gulf, given its alignment with Hamas. For example, threatening to sink or hijack oil tankers. Such a move would undoubtedly cause a substantial spike in the price of oil globally.

That's because the global oil market is a finely balanced one, between supply and demand. Relatively small changes to supply, in percentage terms, cause large swings in the oil price.

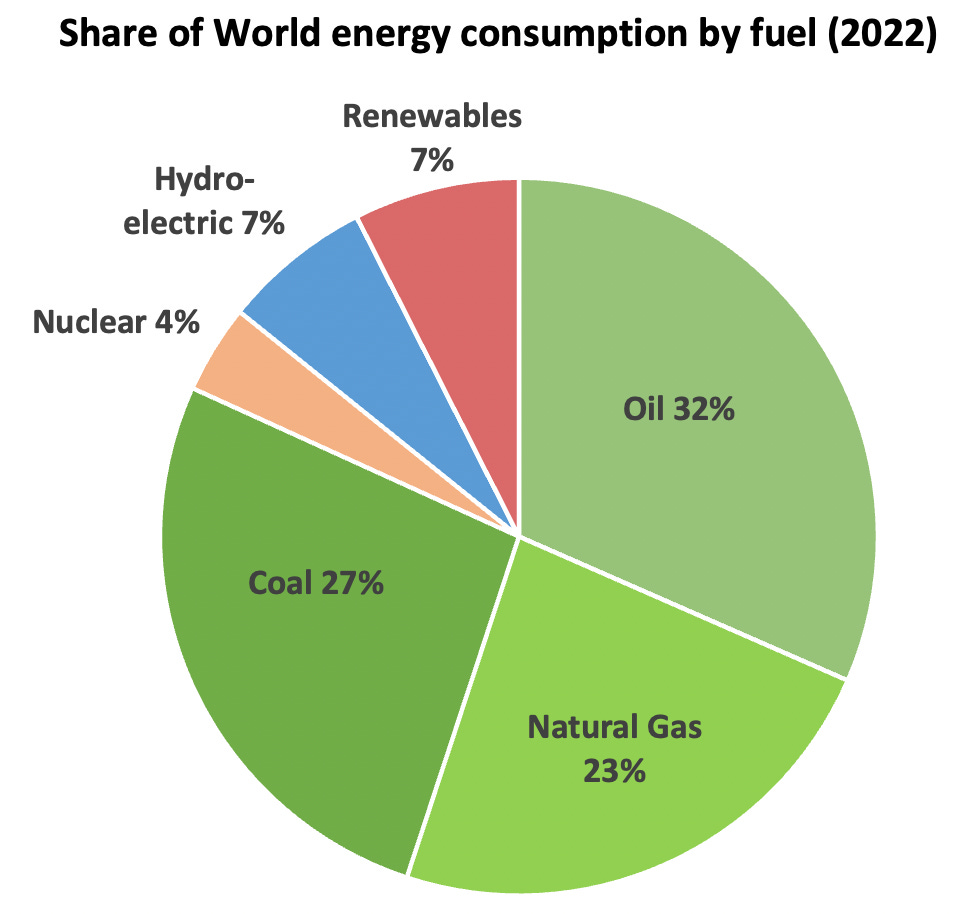

Oil is an essential commodity, both for transport fuels but also for petrochemicals (used to make plastics). In terms of its energy role alone, it delivered 32% of global energy needs in 2022, as shown in the following chart that I knocked up.

Sources: OfWealth, Energy Institute Statistical Review of World Energy 2023.

(Please note the carefully selected and somewhat contrarian colour scheme. While we're at it, please note that combined hydrocarbons - represented in shades of green - provided 82% of total global energy needs in 2022. Hydrocarbons are here to stay for a very, very long time, irrespective of how many people superglue themselves to things or chuck orange paint around. Incidentally, both glue and paint are made from petrochemicals...)

The point is that oil is hugely important, and also that much of it has to be squeezed through the Strait of Hormuz before it reaches global markets, right under the glowering gaze of Iran.

And that's just the shipping side. There's also potential for actual Middle Eastern production of oil (and natural gas) to be disrupted if a wider conflict break outs.

That said, so far at least, the reaction of the oil market has been sanguine. The price of oil has barely reacted to the increased risk of an oil market dislocation (WTI $83.08 and Brent crude $85.93 per barrel).

Why is that?

There are those that ascribe some kind of hive mind genius to financial markets. I am not among them. Markets often get it wildly wrong.

Obvious examples are when the market mob completely failed to see the risks and scale of the forthcoming Global Financial Crisis (2007 onwards), or when investors continued to own bonds with negative nominal or real yields (until the bond market crash started in early 2022).

Of course, I can't know that something bad is about to happen in oil markets. I just think that the risk is much higher than a week ago. All it could take for conflict to spread in the Middle East is one misjudged military order, or one copycat terror attack on a carefully selected target.

While we wait to see how events unfold, this is a reminder of why it pays to own gold.

Or gold mining shares.

Gold is an inflation hedge. If the oil price heads sharply higher for any sort of prolonged period then that will be inflationary, and at a global level.

Gold is also a crisis hedge. Israel and its surrounds are in crisis. That crisis could spread.

Meanwhile, in a country far, far away...

In the meantime, there's a different sort of crisis going on down here in Argentina. A currency crisis.

One of my sisters and her husband were recently visiting, and returned to England on Monday. In the two weeks that we were sampling tango shows together, sightseeing, and eating and drinking too much in the wine region of Mendoza, the Argentine peso lost 14% against the US dollar. It's lost a further 9% in the three days since they left.

At market rates (as opposed to the fake official exchange rate) the peso has lost 66% since the start of the year. Yes, one dollar would buy you a total of 344 humble pesos back in January. Now one dollar can be exchanged for 1,000 of the ever more populous local “store of value”.

That’s quite something when we remember that those two currencies were exchangeable 1-for-1 back in 2001. Put another way, the peso has lost 99.9% of its value, measured in dollars, over the course of 22 years. (And the dollar buys less as well.)

The underlying reason isn't hard to understand. In the twelve months to the end of August, consumer price inflation came to 124%. For the month of August alone it was over 12%. September is also expected to give a double-digit print.

When I moved here in 2008, inflation was in high single digits, or the low teens, if memory serves. For a fellow from England, this seemed outrageously high. Little did I know…

The latest inflationary acceleration is caused by mass money printing to fund the government fiscal deficit. (Sound familiar?) The incumbent Peronist party is adding fuel to the inflationary fire with populist tax cuts and other handouts, ahead of first-round presidential elections on 22 October.

Add in the final frenzy of a heated presidential election campaign, with a lot of finger pointing, and mud-slinging rhetoric hurled between the leading candidates, and it makes for a potent mix of financial uncertainty. The word "hyperinflation" is on more and more lips, and in more and more print.

Anyone with a pulse is dumping pesos and scrambling to get dollars.

Still, at least the sun's shining.

Until next time,

Rob Marstrand

Please send any comments or questions to the following email address:

ofwealth@substack.com

The editorial content of OfWealth is for general information only and does not constitute investment advice. It is not intended to be relied upon by individual readers in making (or not making) specific investment decisions. Appropriate independent advice should be obtained before making any such decision.